When I first moved to the U.S. in 2021, I was paying around $300 a month for health insurance. Given the tax savings compared to Canada, and the fact that you can actually get care quickly here, I didn’t bat an eye.

But fast forward three years and that same plan had climbed to $450 per month, with a higher deductible, worse coverage, and a growing sense that I was throwing money away. After all, I’m in very good health and hardly ever use the healthcare system.

Fortunately around that time, I heard about CrowdHealth while listening to a podcast. The concept instantly clicked — a low monthly cost and “coverage” only in case of emergencies. You know… like what health insurance is actually supposed to be.

I was intrigued enough to dig deeper and eventually decided to take the plunge. After having a good experience, I later brought my family along with me.

In this CrowdHealth review, I’ll share how it works, what my experience has been so far, and whether it’s truly a viable replacement for traditional health insurance.

What is CrowdHealth?

At a high level, CrowdHealth is a community-based alternative to traditional health insurance. It’s not an insurance company — there are no networks, no deductibles, and no confusing policies. Instead, members pay a flat monthly amount, and when someone in the community has a medical bill, everyone chips in to help pay it.

Think of it like a modern version of people pooling money to help each other out, except the entire process is handled through an app.

How CrowdHealth works

CrowdHealth takes a refreshingly simple approach to handling medical costs. Once you understand the basic structure, it’s easy to see how the model keeps expenses low.

Here’s how it works in practice.

1. The monthly advocacy fee

This is essentially your subscription fee for being part of the CrowdHealth community. It covers things like the app, member support, and the team that negotiates and coordinates medical bills on your behalf.

Right now, the advocacy fee is $60 per month per person. You pay this directly to CrowdHealth every month, just like any other subscription.

2. The monthly contribution

In addition to the advocacy fee, you’ll also receive funding requests each month from other members who need help paying medical bills.

You simply keep a credit card or payment method on file, and when you approve a request, CrowdHealth automatically charges your card for your share of that bill.

You can also set up auto-approvals for “green” bills — these are expenses CrowdHealth has reviewed to confirm that the cost is fair and the member submitting the bill has a solid generosity score (more on that below).

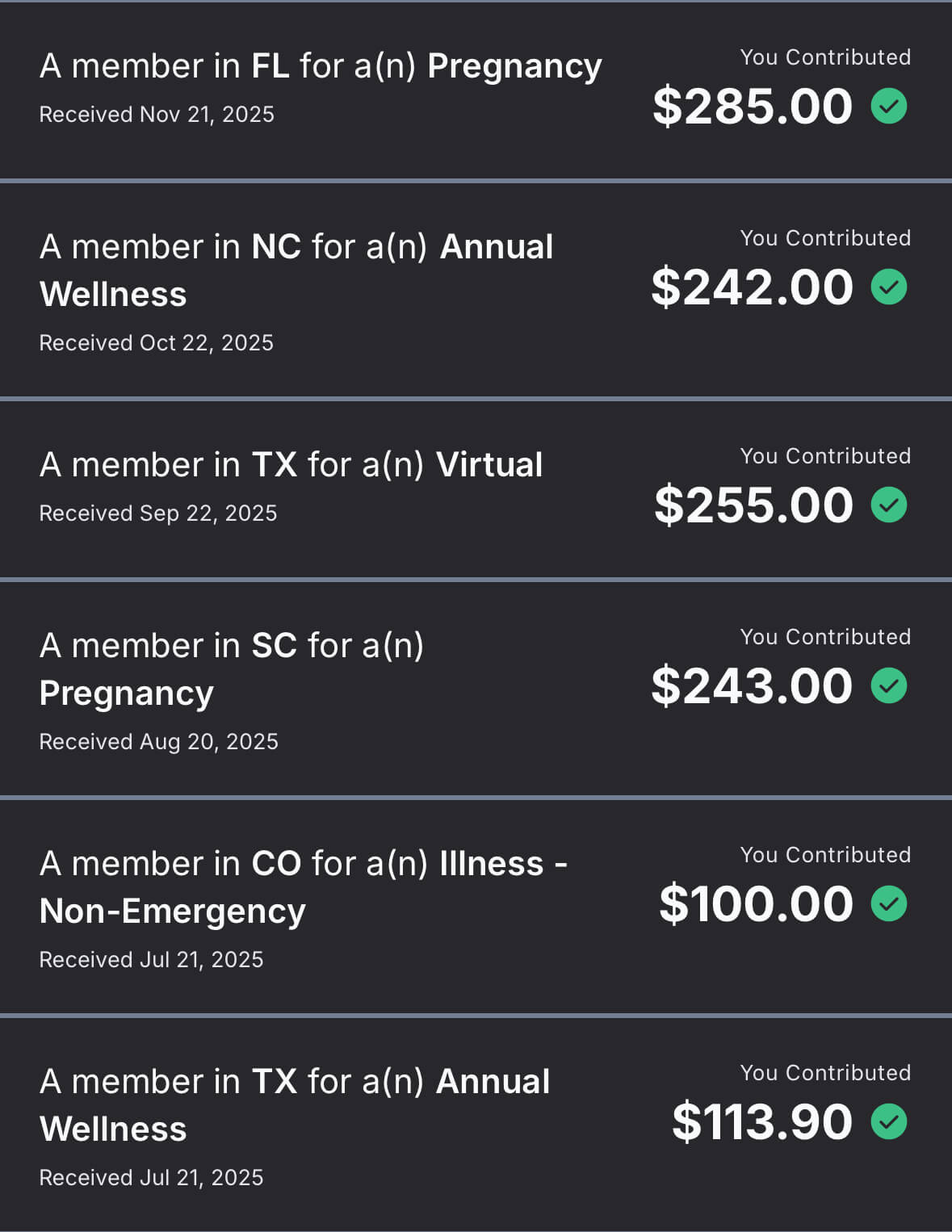

When a funding request comes in, you’ll see what the expense was for (e.g., “ER visit after bike accident”) and how much you’re being asked to contribute. Once you approve it, that money goes directly toward helping pay that person’s medical bill.

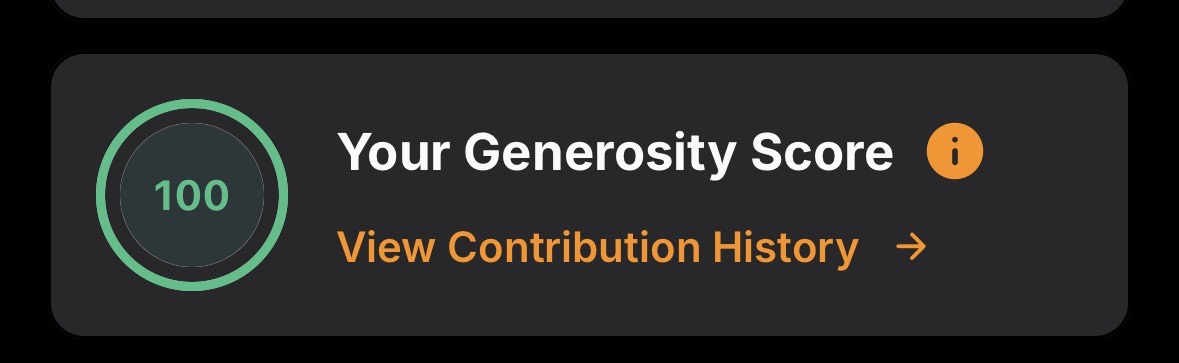

3. The generosity score

Your generosity score tracks how consistently you participate in funding other members’ bills. Keeping it in the green (ideally 100%) means you’ve been reliable in contributing when requests come in.

Ignoring too many requests lowers your score — and that can affect both the speed and likelihood of your own bills being fully funded.

Essentially, the generosity score is a smart way to keep the model functioning properly. Everyone is incentivized to continue funding other bills, so in turn they’ll have no issues getting their own bills funded.

4. Paying and submitting medical bills

For smaller medical expenses under $500, you simply pay out of pocket.

Once a bill goes over $500, you can upload it through the CrowdHealth app for funding. The CrowdHealth team reviews it to make sure it’s legitimate and fairly priced before it’s sent out to the community.

For larger or scheduled procedures, CrowdHealth asks that you contact them beforehand. Their team can help find a provider who charges fair, market-based prices. In many cases, they’ll coordinate crowdfunding in advance so the funds are available by the time of service.

Bills marked as “green” indicate two things: your generosity score is solid, and the cost of the procedure is within a reasonable market range. That helps other members feel confident funding it.

When your bill is fully funded, the entire amount is deposited into your bank account, and you pay your provider directly.

5. $300 annual wellness allowance

Although smaller bills are paid out of pocket, you do get $300 per year for wellness expenses. This can be used for things like annual checkups and bloodwork.

You can even use it for dental cleanings and X-rays, which is how I’ve been using mine.

Comparing costs: CrowdHealth vs. traditional insurance

One of the biggest reasons I decided to give CrowdHealth a shot was the cost difference. Traditional health insurance premiums have gotten completely out of control, and the coverage you get for that price just keeps shrinking.

This became an even bigger concern after my wife and I welcomed our son earlier this year and suddenly needed coverage for a family of three.

For context, the cheapest Florida Blue plan available for my wife, child, and me in 2026 costs $1,328 per month. That plan comes with:

- $7,400 deductible per person ($14,800 per family)

- $9,950 out-of-pocket max per person ($19,900 per family)

That means, in a typical year with no major health events, we’d be paying $15,936 in premiums alone — before even touching the deductible.

By comparison, here’s what we pay for CrowdHealth:

- Advocacy fee: $60 × 3 = $180/month

- Max monthly contribution: $140 × 3 = $420/month

- Total monthly cost: $600

That’s less than half the cost of the cheapest traditional plan. Over the course of a year, that’s $7,200 total, compared to nearly $16,000 for Florida Blue.

Also, that’s assuming the full monthly contribution. And since I’ve been a member, that virtually never happens. Looking back at my own funding history, the monthly contribution is usually $50 less per person.

So in reality, we’re paying closer to $450 per month, depending on how many community bills come through.

Even if we stop there, the savings are huge — around $10,000 per year for a typical year with no major medical events.

But the difference becomes even more extreme in a worst-case scenario. If multiple people in our family had a major medical event that maxed out our deductible and out-of-pocket costs, here’s what that would look like:

- Florida Blue: $15,936 in annual premiums + $19,900 in out-of-pocket costs = $35,836 total

- CrowdHealth: Around $6,000 total, with anything above the first $500 per event funded by the community

That’s almost $30,000 in potential savings in a single year.

Of course, CrowdHealth isn’t insurance, so there are some caveats which I’ll touch on below. But purely from a financial standpoint, it’s hard to ignore how much better this model is.

My experience with CrowdHealth so far

When I was first considering joining CrowdHealth, I booked a call with a member of their team. They were super helpful in answering all my questions and walking me through how the model works and what to expect as a member. After that call, I decided to sign up. The entire onboarding process was smooth and straightforward.

When I first joined two years ago, I signed up just for myself. I wanted to test it out and see how it worked in practice before making any bigger commitments. After a consistently positive experience, I decided to move our whole family over partway through this year.

Fortunately, I haven’t had any major health events since joining, so I’ve yet to submit a bill over $500 (and hopefully won’t have to anytime soon). However, I’ve made use of the $300 annual wellness allowance by submitting my dental cleaning and X-rays for the past two years.

Submitting bills has been simple and painless. You just take a photo of your receipt and upload it through the app. Both times, I was reimbursed in less than a month without any issues. My wife had the same experience using her annual wellness allowance this year.

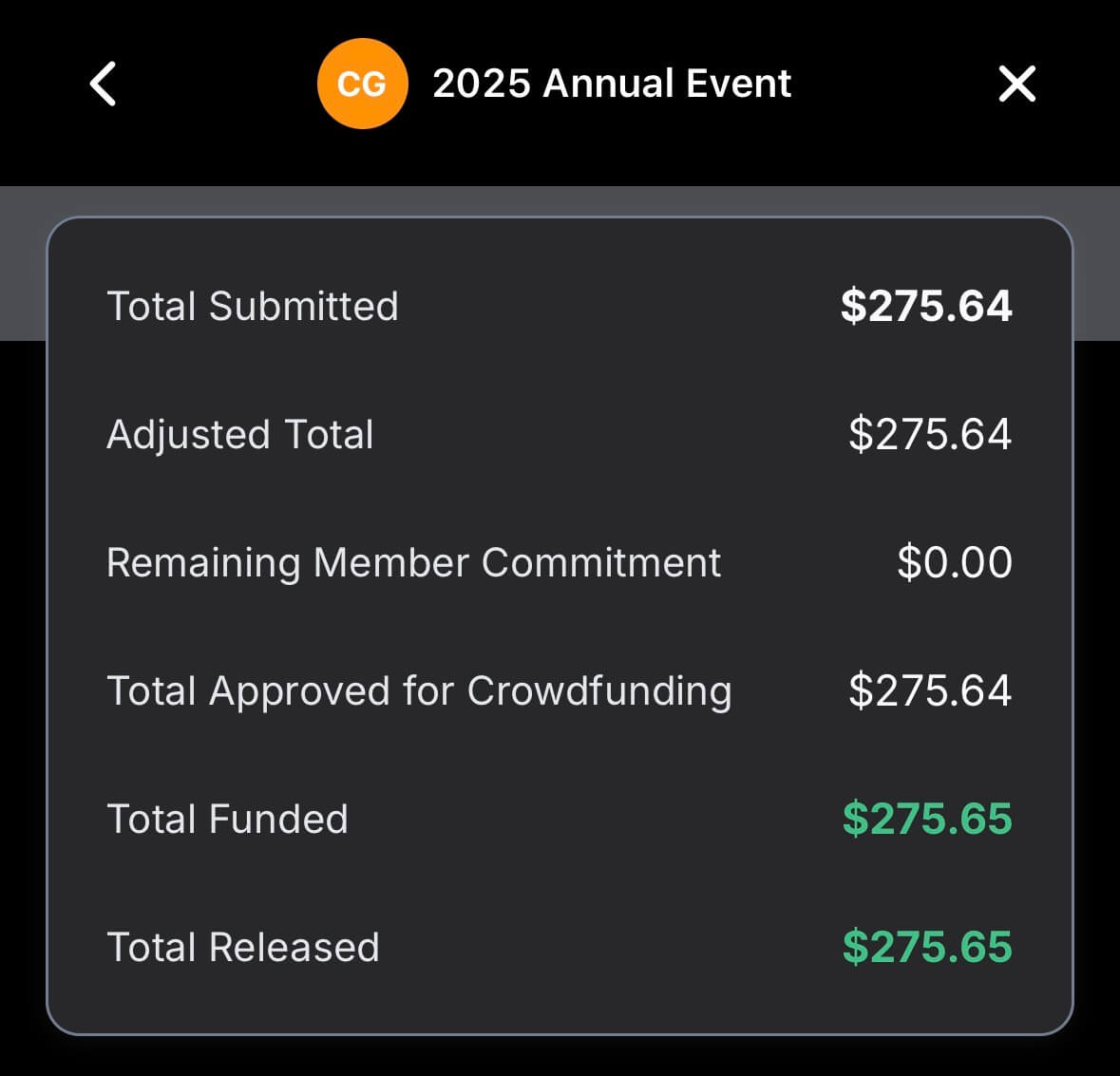

Best of all, the monthly contribution requests have consistently come in below the max amount. Since signing up our family of three, our monthly contribution has averaged $254 per month ($85/person).

This ends up being $2,000 less each year than what we’d expect to pay at the full contribution level!

What’s the catch?

At this point, you might be wondering what the catch is. CrowdHealth isn’t traditional insurance, so it naturally comes with a few important caveats.

1. Pre-existing conditions aren’t covered right away.

CrowdHealth doesn’t fund bills tied to pre-existing conditions during your first two years as a member. After that waiting period, those conditions are treated like any other expense. This policy keeps costs fair for everyone and helps prevent people from joining only when they already know they’ll need expensive care.

2. You’re asked to contact CrowdHealth before scheduled procedures.

If you’re planning a surgery or another major procedure, CrowdHealth asks that you call them first. Their team can help find a doctor who charges fair, market-based prices and negotiate rates on your behalf.

If you don’t contact them first and end up submitting a bill that’s well above the market price for that procedure, that information is displayed to members when it’s time to fund your bill — which could impact your bill getting funded.

3. It’s not insurance — and that’s both a pro and a con.

Since CrowdHealth isn’t technically insurance, there’s an element of trust built into the model. But they’re extremely transparent: you can view every single bill ever submitted for crowdfunding on their website — including whether it was funded or not.

As of now, 99.9% of bills have been funded, and the rare exceptions typically fall into two categories:

- Bills related to a pre-existing condition within the first two years of membership.

- Bills that were significantly higher than the market rate for that procedure.

4. There are some eligibility requirements.

CrowdHealth doesn’t currently accept members who smoke or whose weight exceeds 220 lbs for women or 260 lbs for men. Personally, I view this as a positive, since both smoking and obesity are major contributors to higher healthcare costs.

By focusing on healthier members, CrowdHealth helps keep monthly contributions low for everyone. And since both smoking and maintaining a healthy weight are largely lifestyle choices, this approach feels fair and sustainable for the long term.

Lastly, it’s worth noting that CrowdHealth doesn’t qualify as insurance in certain U.S. states due to local mandates. Fortunately, that’s not an issue in Florida where I live, but it’s something to check if you’re in a state with stricter insurance requirements.

Final thoughts

So far, I’ve had a very positive experience with CrowdHealth. The team has been friendly, the onboarding was seamless, and I’ve had no issues submitting bills or getting reimbursed for my wellness visits.

The only thing I can’t fully vouch for yet is reimbursement for a medical event over $500. But since my wife and I are planning to have more kids, I know that day will eventually come. When it does, I’ll be sure to update this review.

In the meantime, we’re happy to be saving $10,000 per year on premiums alone.

If you’re curious to learn more or ready to ditch traditional health insurance, you can check out CrowdHealth here. By signing up with my referral code (WC5WXU), you’ll also receive a discount, bringing your total to $99/month for the first three months.